1. Car Ownership Dreams and the Need for Good Financial Management Skills

Car buying is usually associated with some of the most memorable events in people’s lives. Owning a car stands for freedom, independence, and self-realization. There is nothing more exciting than visiting a car dealership, feeling that fresh car aroma, and holding the keys of your new car. But while all the fun of this purchase should not be underestimated, the financial obligations associated with it shouldn’t either. To go from dreaming about owning a car to actually purchasing one, proper financial planning is required.

However, the process is quite risky if you do not prepare well for it. This is when vehicle financing becomes handy. Being aware of what kind of vehicle one can purchase and what he or she cannot afford is a critical aspect of good personal finance management. There is nothing unusual about people going to buy vehicles without a budget. Such behavior leaves customers defenseless because sales people concentrate only on the current situation instead of its consequences for the future. However, using an auto loan calculator proves to be very useful if you want to purchase a car responsibly.

2. Auto Loan Calculator Definition

An auto loan calculator is a specially-designed program that enables individuals to calculate the amount of money they’ll be spending in the future while buying a car using a loan. Essentially, the most fundamental objective of an auto loan calculator lies in simplifying the complicated mathematical equations involved in loan amortization to give you a clearer picture of the financial commitment you’re making. With an auto loan calculator, you can perform complicated mathematical equations without effort.

How does a car loan calculator work? Well, it is pretty simple yet very effective. It utilizes the conventional amortization formula to know what portion of your payment is going into the principal value and what part is being used to pay off the interest. You have to provide certain pieces of information, such as the total value of the car, how much money you are willing to deposit initially, the period of time for which the loan would be taken out, and also the interest rate on the loan. The data is then processed and an accurate idea of your regular costs is produced. Hence, it allows you to know the true value of your automobile, without having to take a guess at it.

3. Detailed Steps on How to Utilize the Calculator

To obtain highly accurate figures using an auto loan calculator, it is essential to understand the purpose of each data input field. The following guide highlights all necessary fields that will require careful evaluation.

1. Vehicle Cost

This figure represents the total cost associated with purchasing the car. In most cases, it will refer to either the Manufacturer’s Suggested Retail Price (MSRP) for brand new vehicles or the sticker price for second-hand vehicles. To be more precise, it is important to provide the actual price, which may be different from what was originally advertised due to negotiation practices.

2. Initial Payment

The initial payment refers to the upfront amount of money paid by the buyer during the acquisition of the vehicle. By increasing this number, one will be able to reduce the total amount of borrowed money, which will reflect positively on subsequent payments and long-term expenses. When trading in the old car, this number is calculated together with its trade-in value.

3. Loan Duration

This is how long you will take to repay the loan amount in full and is measured in months. A usual term may be anywhere between 36, 48, 60, up to 72 months. This option selected on the calculator affects the size of your monthly payments tremendously.

4. Interest Rate (APR)

Interest rate, also known as annual percentage rate (APR), is the fee for using the money provided to you, shown per year. It consists of the actual interest on your loan and any other fees the lender might charge. Getting an advantageous interest rate is the key aspect of reasonable car financing because the small change can save thousands over time.

4. Rates of Interest – Fixed and Variable Rates, and How Your Credit Score Affects Them

It is important to understand the way interest rates work before obtaining any vehicle loan. The interest rate determines the additional cost you have to pay the lender for using their funds. When you make use of an online auto EMI calculator, the interest rate happens to be the most dynamic factor that needs consideration.

Fixed Interest Rate vs. Variable Interest Rate

- Fixed Interest Rate: The great majority of car loans operate on fixed interest rates. It implies that the interest rate will stay unchanged throughout the term of the loan. The main benefit of fixed interest rates is that your monthly payments cannot change at all.

- Variable Interest Rate: Such type of interest rate depends on the base rate of interest in the market. If the interest rate goes down, then you will be paying lower amounts. Otherwise, you will be forced to pay higher amounts. Variable interest rates are usually riskier than fixed ones.

Fixed Vs Variable Interest Rate

- Fixed Interest Rate: Most car loans come at fixed interest rates. This implies that the interest rate is not going to change for the duration of the loan period. The main benefit of fixed interest is its predictability. You will always know what amount your monthly car payment will be.

- Variable Interest Rate: The rates depend on the underlying interest rate. If the interest rate decreases, you pay less, but if it increases, you have to increase your payments accordingly. The disadvantage of variable interest rates is their unpredictability. It can be risky for people who are buying cars with a plan of keeping them longer than the initial loan period.

The Effect of Your Credit Rating

Credit rating is the most critical aspect that lenders consider when offering loans. They perceive the credit history of the borrower as a certain measure of risk.

- Excellent Credit Score: Those borrowers, who can boast high credit scores, get low interest rates, thus decreasing the total cost of the loan.

- Poor Credit Score: Poor borrowers’ credit history makes them high risk; therefore, the interest rates offered are quite high, increasing dramatically the total price of the car.

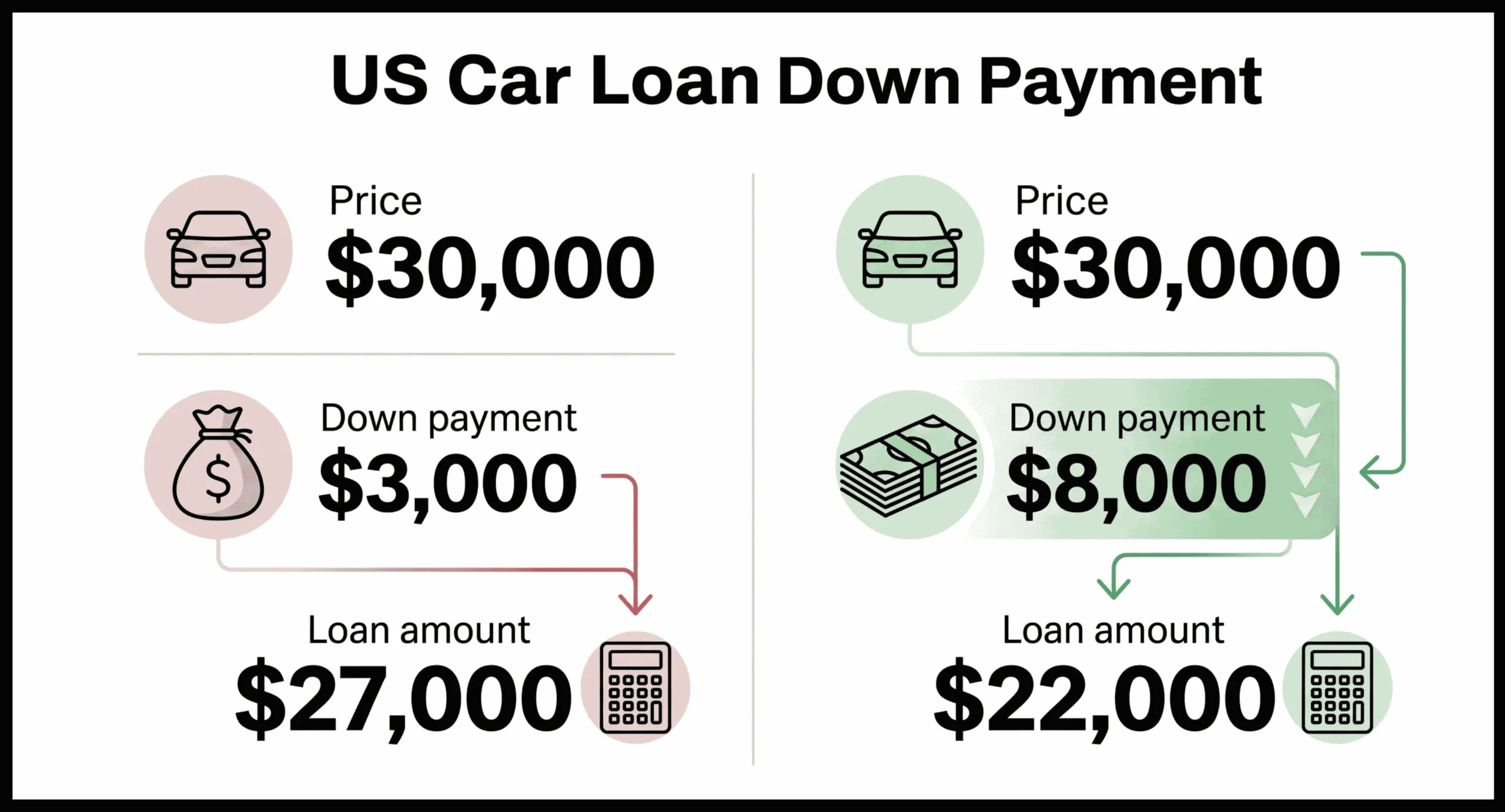

5. The Importance of Down Payment

It may come as a surprise to many individuals that there is great financial power behind the down payment amount. A large down payment is one of the best options for ensuring that you save a lot of money in your automobile financing process. The amount of down payment determines the principal balance of your loan.

The moment you increase the amount of the down payment entry in your auto loan calculator, there will be a positive impact on all other parameters. The first positive thing about increasing the down payment is reducing your monthly car loan payment, making it easier for you to use your money elsewhere. The second aspect, which is even better, is that it will reduce the amount of interest that you pay throughout the duration of your loan.

In addition to this, a good down payment prevents you from being “underwater” or “upside-down” on your car loan – when the value of the vehicle drops below the amount you have remaining to pay on it. Because vehicles depreciate rapidly, by 20% within the first year or more in some cases, the initial payment cushions you against this depreciation and ensures that you do not start out in debt from day one with regard to the value of your new car.

Scenario:

- Price of car: $30,000

- Down Payment: $3,000 – Resulting loan: $27,000

- Down Payment: $8,000 – Resulting loan: $22,000 and thousands of dollars saved on interest

A minimum down payment of 10% is advised for second-hand vehicles while 20% is recommended for brand new cars.

6. How Long Should the Loan Be? 36 Months? 72 Months?

Deciding which loan term suits you best requires balancing affordability of the monthly payments and the total cost of borrowing. Your choice of loan term in the auto loan calculator greatly affects your financial situation for many years after making your decision.

Short-Term Loans (for example, 36-48 months)

- Advantages: The main advantage of such a loan term is that in total, you will be paying a lot less interest. Secondly, building equity in your car goes much faster, which means that you own the car fully sooner.

- Disadvantages: As the loan term is reduced, so does the number of payments, thus increasing the amount of the car loan monthly payment. It requires extra disposable cash in your budget.

Long-Term Loans (for example, 72-84 months)

- Advantages: Increasing the loan term means that the principal amount will be paid back over a greater period of time; therefore, the monthly car payment will become much smaller. This is often attractive when buying an expensive car where monthly expenses cannot be too large.

- Disadvantages: The disadvantages of a long-term loan are considerable. In total, you pay a lot more interest, and you significantly increase your chances of getting into negative equity. As the car depreciates much quicker than the principal is being repaid, you will end up owing money for some time on a car that is already not worth that much anymore, making selling it a difficult task.

Financial Knowledge Tip:

- For the same car, a 36-month loan will cost about $3,000 in interest payments

- A 72-month loan will cost approximately $6,500 in total interest

Compare various scenarios using an auto loan calculator to determine the best choice.

7. Other Cost Factors of Purchasing a Car

Depending only on the principal and the interest when making a budget is risky. To make a correct estimation of vehicle financing, one should take into account the additional costs that cannot be avoided. Even though an auto loan calculator is useful for calculating the payment terms, the list of factors includes other aspects.

- Taxes: You need to pay a certain percentage from the price of the car to the government. Taxes can range thousands of dollars and can be included in the amount of a loan or paid separately.

- Registration and Title Fees: The fees necessary for legal registration of the car under your name. Depending on the place where you live and the car type, the sum may differ.

- Insurance: It is a must to have both comprehensive and collision insurances during the whole period of the loan. The cost depends on the type of the vehicle, your driver experience, and many other factors.

- Repairs and Maintenance: Oil and tires change, brake pads, and other regular car maintenance costs need to be accounted for.

- Depreciation: It is an inevitable factor for cars. Depreciation is especially significant at the beginning of your car’s life span.

8. Comparison Between Leasing and Purchasing a Car

Individuals may sometimes find themselves between a rock and a hard place regarding whether to lease or buy a car. There are pros and cons involved in both options, and use of an auto EMI calculator helps you make up your mind based on your personal finances.

Buying a Car

If you choose to buy the car through an auto loan, you will pay towards its ultimate ownership. Once the loan is paid off completely, you get the title, thus owning it without a mortgage. You can drive as much as you like, alter the car according to your needs and sell it. The disadvantage of buying a car is that its monthly payments will be higher compared to when you lease the same model. Also, you pay for its full depreciation.

Leasing a Car

Leasing is simply a temporary form of rental. Here, you will only pay for its depreciation and not for the total purchase price, hence lower monthly payments. If you want to drive a new car after a certain period and enjoy it being still under the manufacture warranty, you should consider this option. Its downside is that it has mileage restrictions, and once the contract ends, you will have no asset since you will have to give back the leased car.

Through use of an auto loan calculator, you can analyze your decision mathematically.

9. Common Mistakes People Make When Financing Cars

When buying a car, there are several mistakes people make that cause them to lose a lot of money. Understanding these mistakes will help prevent them from making similar mistakes.

1. Focusing on Monthly Payments Only

The most common mistake in the process of financing vehicles is concentrating only on monthly payments. Dealers tend to stretch loans for customers to achieve their monthly targets. Although monthly payments look cheaper, they result in high interest costs. Ensure to utilize auto loan calculators when evaluating loan options.

2. Failure to Obtain Pre-Approval for the Loan

Some people buy cars from dealers without seeking outside sources of financing. In this case, people end up financing vehicles based on dealers’ interest rates, which may not be the best option. It is always wise to obtain pre-approval from banks and credit unions before going to the dealership.

3. Financing Negative Equity

Some lenders will allow you to finance negative equity during vehicle financing. This means that if your trade-in vehicle has negative equity, you can finance it together with the new car. However, it would be best not to finance negative equity since you increase the loan principal amount.

4. Financing Without Making Any Down Payment

Some dealers will offer low-interest rates or special terms when financing vehicles for people who do not make any down payment. Avoid financing without down payment because it results in increased total interest cost.

5. Obtaining Auto Financing Without Checking Credit Score

The credit score plays a critical role in obtaining car financing. Therefore, it is important to check and evaluate your credit score before applying for vehicle financing.

10. Auto Loan Refinance: Exploiting Rate Reductions

The arrangement of auto financing is not a static one, which implies that you can renegotiate the terms of repayment in case of favorable changes in market conditions. A refinance is defined as getting a new loan to pay off your previous auto loan, with the hope of getting better terms.

In case the interest rates offered by the central bank fall drastically, or there is an improvement in your personal credit score after buying the car, then you should consider refinance. You can get a better interest rate, thereby reducing your monthly car payment, saving money by paying less interest over the lifetime of the loan. Using the online auto loan EMI calculator can help you determine whether the refinance is beneficial. All you need to do is enter the outstanding principal amount in the online calculator and compare your current interest rate with the new offers available in the market. You will be able to calculate the breakeven point and see how much you save in the long run from refinancing.

You can refinance if:

- Interest rates fall in the market

- There is a significant improvement in your credit rating

- You earn more

- Your goals change

It is important to consider the refinance fees and the balance of your loan at the time of doing so.

11. Auto Loan vs. Personal Loan: A Comparison

While applying for auto loans, consumers often question whether using a regular personal loan to buy a car would be better than using an auto loan. The fundamental difference between the two types of loans is the existence of collateral.

An auto loan is a type of secured loan. In this arrangement, the car is used as security for the lender. If you default on repayments, the lender may seize your car. Since the lender faces minimal risks, interest rates are relatively low on auto loans.

On the other hand, personal loans are usually unsecured, implying that they lack collateral. Thus, the lender has a high-risk portfolio and, as a result, offers personal loans with relatively high-interest rates.

Check out our other calculators

Want more tools to help you with your money? Use our free calculators to help you make better financial choices:

Our Interest Calculator will help you understand how interest rates affect your monthly payments.

Are you planning to buy a home? You can use our Mortgage Calculator to figure out how much your monthly house payments will be.

Need a tool for general financing? For all your borrowing needs, use our Loan Calculator.

Start making better decisions with accurate figures. Try our free online calculators now.